Imagine, you are on a vacation to Maldives. Mesmerizing view of the ocean from the beach house in Maagau Island seems overwhelming. Filled with joy and a heart with desire to stay longer, dwelling into the noises of the water and air make when they collide. The night music with salsa dance and a sea food buffet to fill it all that a vacation requires.

Now, that you know what it feels like to meet heaven on earth and if you are a U.S. Citizen or a Green Card Holder, you don’t need a Visa to travel to more than 100 countries in the world.

Now, think of the taxes that you pay the U.S. Government from your earnings and the benefits you can reap from those even if you don’t pay a penny. Not sure how they are processed! Here is a quick overview based on your circumstances, how to file as an individual:

- Single

If at the end of the year you are considered unmarried, file as a single individual even you were married at some time during the year.

Do keep in mind that if you divorced your spouse the year you file your returns as single and marry again the following year as a married individual jointly or separately, you are not eligible to your single status the previous year for tax purposes. File Form 1040-X to amend your Tax Return Filing.

- Married Filing Jointly

If at the end of the year you are considered married, file as Married Filing Jointly in your Form 1040 Individual Tax return. In this filing status, couples can report their combined incomes, expenses, assets, deductions, and credits. Your spouse must be willing to file jointly for that matter.

A special consideration is made for taxpayers who lost their spouse to death. If during the year your spouse passed away, you can still file jointly that year including the following 2 years.

Your spouse died during the year 2021, you can file as MFS for 2021, 2022 and 2023 as per special consideration by the IRS.

Filing a joint return means sharing the responsibility as one, in terms of exclusions, credits, and liabilities as well. If one of the spouses is flagged by the IRS for Tax Fraud or with any other criminal activities, the other spouse is equally responsible for the blame. Same goes for taxes due of any one spouse that is enforced on both.

There are few reliefs that a spouse can claim in terms of separation of fault, which are:

- Innocent Spouse Relief

- Separation of Liability

- Equitable Relief

- Married Filing Separately

Married individuals can file separately if they want to or qualify. This is where all their income, expenses, assets, deductions, liabilities, and credits are reported and claimed on separate returns even when married.

It is rare to come across this filing for married individuals that have a combined income of less than $500,000. It also has the lowest requirement to file for taxes if the income is $5 or more.

This filing status is considered for high income earners in general, for those who are married and want to file their annual tax returns separately. In this case, you would pay higher tax rates compared to Married Filing Jointly, as it has the lowest tax rates for individuals.

You can also file as Head of Household if you have not lived with your spouse for a certain period and meet other certain tests. The other spouse can file separately as it will be the only option for them.

It is better to calculate your taxes both ways with the help of a tax professional if needed before filing for a particular status.

- Head of Household

This filing status has the second highest standard deductions after MFJ. You are considered single or filing separately if on the last day of the year to file as Head of Household.

- To qualify as single or considered unmarried certain criteria is to be met:

- You file a separate return.

- You paid more than the half of the cost of running your home for the tax year.

- Your spouse did not live in your house for the last 6 months of the tax year. Temporary absence of your spouse is also considered as living in the house.

- It was the main home of your child, stepchild, or foster child for more than half of the year.

- You must be able to claim the child as dependent. This requirement is fulfilled even when you cannot claim the child as dependent if the non-custodial parent claims the child as a dependent on his/her tax return.

- You paid more than the half of the cost of running your home for the tax year.

- A person that qualifies as a dependent has lived with you for more than half of the tax year. However, if the qualifying person is your dependent parent, he/she does not have to live with you to claim them as dependents.

This method can save you more in taxes paid to the US government or none at all for the tax year. It is advised to get professional help before filing your taxes to work all possible tax reducing methods and apply the best outcome.

- Qualifying Widow(er):

If your spouse died during the year 2021, you can use the MFJ status but before that you may have to file as a Widow(er). This is the last time you can file joint returns with your spouse. There is another way to file as Married Filing Jointly for the following 2 years from the year when your spouse died, where you have to meet certain criteria to be eligible:

- You filed joint returns for the tax year when your spouse died.

- You did not remarry during the following two years from your spouse’s death.

- You have a dependent child or stepchild or both, excluding foster child.

- The child that you will claim as dependent has lived with you all year except temporary absences.

- You must have provided more than half of the total cost in keeping up the home in which you and your claimable dependent child have lived. Expenses include the mortgage or rent payments, property taxes, utility bills and groceries.

All the above criteria are to be met to be eligible as a qualifying widower. If you remarried during the above said duration for which you could file as a Qualifying Widow(er), the year you remarry, you won’t be able to file your annual tax return(s) as a Qualifying Widow(er).

Example: Harry lost his wife in 2021 and remarried in 2024. He qualifies to file his 2021 tax returns as Married Filing Jointly or Separately. He has a daughter aged 8 years old for whom he bears all costs for the tax year. For the following 2 years (2022 & 2023) he may qualify to file as a Qualifying Widow(er) with a Dependent Child, claiming the tax benefits of joint filing. Harry will only be eligible for the Qualifying Widow(er) status if the child is claimed as a Dependent Child. Harry can claim the Qualifying Widow(er) status for 2022 and 2024 and claim MFJ or other applicable status for 2024 onwards with his new partner.

If john had remarried before January 1, 2024, he could not have claimed the Qualifying Widow(er) status for the year he got married and onwards.

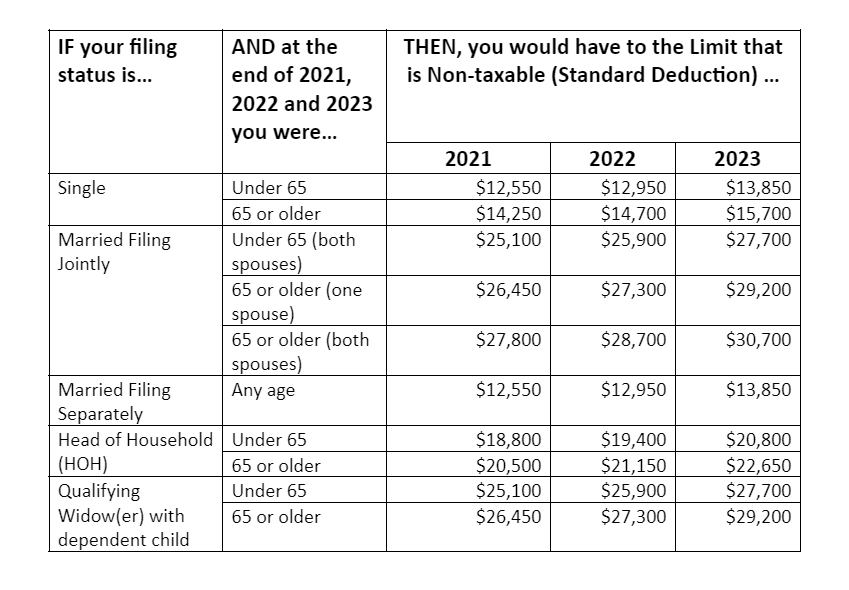

Standard Deduction

The U.S. government has allowed a minimum non-taxable income for U.S. persons for each type of status available for Individuals. Following are the exclusions that are available

You are required to file for a U.S. Annual Individual Tax Return Form 1040, if your income exceeds the standard deduction threshold per filing status except for Married Filing Separately, where you will have to file a tax return if income exceeds $5, but taxable on the remaining income after the standard deduction has been claimed.

An additional exclusion can be taken for individuals who are blind or at least aged 65 or both. The exemptions are as follows:

- Married Individuals (Filing Jointly and Separately):

If the taxpayer at the end of the year 2021, 2022 or 2023 is a married individual and is at least aged 65 or blind can claim an additional $1,350, $1,400 or $1,500 in standard deductions or aged 65 and blind can claim twice of $1,350, $1,400 or $1,500, resulting to a whopping $2,700, $2,800 or $3,000 deduction or a refund.

- Single and Head of Household:

If the taxpayer at the end of the year 2021, 2022 or 2023 is Single or Head of Household and is at least aged 65 or blind can claim an additional $1,700, $1,750 or $1,850 with standard deductions or aged at least aged 65 and blind can claim twice of $1,700, $1,750 or $1,850, resulting to a deduction or a refund of up to $3,400, $3,500 or $3,700.

Anything earned above these standard deductions would qualify being taxed at various rates for each applicable status.

Frequently Asked Questions:

- Do I have to file taxes if my earning is less than Standard Deduction?

The IRS does not require it to file Annual Tax Returns, if you earn less than the Standard Deduction for any filing statuses except for Married Filing Separately.

Married Filing Separately is required to be filed if income exceeds $5 for any age Individual whether you live in the U.S. or abroad.

It is recommended to file your Annual Tax Returns for any refundable credits that you may be eligible to claim and also being compliant year to year even though you may not be required to do so. Consult with a tax professional for a better understanding.